{kind=link}

Unlocking Financial Potential: The Dynamics of Cash Value in Insurance Policies

In the realm of insurance, the term “cash value” takes center stage, representing a unique financial component that goes beyond traditional coverage. This comprehensive guide aims to demystify the concept of cash value, exploring its significance, how it differs across insurance types, and the strategic role it plays in financial planning.

Understanding Cash Value

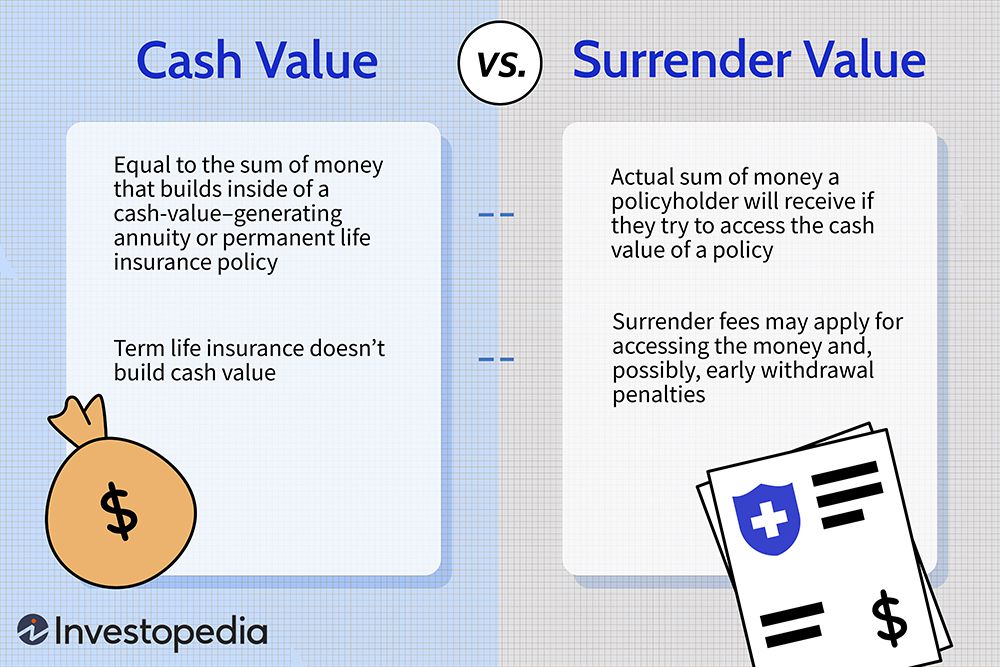

Cash value, often referred to as the cash surrender value, is a feature found in certain types of life insurance policies. It represents the savings or investment component of the policy, allowing policyholders to accumulate funds over time. Unlike the death benefit, which is the primary purpose of life insurance, cash value provides a tangible monetary value that policyholders can access during the life of the policy.

Types of Life Insurance with Cash Value

Several life insurance policies incorporate a cash value component. Understanding these types provides insights into how cash value operates within different insurance structures:

- Whole Life Insurance: Known for its lifelong coverage, whole life insurance policies accumulate cash value over time. This cash value grows at a guaranteed rate and is tax-deferred, offering a source of savings that policyholders can access through withdrawals or loans.

- Universal Life Insurance: This policy provides flexibility in premium payments and death benefits. The cash value in universal life insurance is linked to market interest rates and can fluctuate based on the performance of underlying investments.

- Variable Life Insurance: Similar to universal life insurance, variable life insurance allows policyholders to invest the cash value in a range of investment options. The cash value and death benefit depend on the performance of these investments.

Significance of Cash Value

The inclusion of cash value in life insurance policies adds a layer of financial versatility. Key aspects of its significance include:

- Savings and Investment: Cash value serves as a vehicle for savings and investment within the life insurance policy. It allows policyholders to build a fund that can be accessed for various purposes.

- Policy Loans: Policyholders can take out loans against the cash value of their policies. These loans accrue interest but provide a means for accessing funds without surrendering the policy.

- Withdrawals: Cash value can be accessed through withdrawals, providing liquidity for policyholders in times of need. Withdrawals may impact the death benefit and could have tax implications.

Factors Influencing Cash Value Growth

Understanding the factors that influence the growth of cash value is crucial for policyholders seeking to maximize this component:

- Premium Payments: The amount and frequency of premium payments directly impact the growth of cash value. Consistent and higher premium payments contribute to faster cash value accumulation.

- Policy Type: Different life insurance policies offer varying rates of cash value growth. Whole life insurance policies typically provide more stable and guaranteed growth compared to variable or universal life insurance.

- Market Performance: For policies tied to market performance, the overall performance of the financial markets can influence the growth of cash value. Policyholders assume a level of risk associated with market fluctuations.

Strategic Considerations for Policyholders

Maximizing the benefits of cash value requires strategic planning. Policyholders should consider:

- Balancing Premiums: Striking a balance between affordable premiums and substantial cash value growth is crucial. This involves aligning premium payments with financial goals and capabilities.

- Understanding Policy Terms: Policies vary in terms of surrender charges, interest rates on policy loans, and withdrawal rules. Understanding these terms is essential for making informed decisions.

- Integration with Financial Goals: Cash value can be a valuable asset in achieving financial goals such as funding education, supplementing retirement income, or addressing unexpected expenses. Integrating cash value growth into broader financial planning is key.

Cash Value in the Digital Age

The digital age has brought about advancements in policy management and access to cash value information. Online platforms and mobile apps provide policyholders with real-time visibility into the growth of their cash value, enhancing transparency and control.

Conclusion: Empowering Financial Futures with Cash Value

In conclusion, cash value represents more than just a financial component within life insurance; it’s a tool for financial empowerment. By understanding its significance, factors influencing growth, and strategic considerations, policyholders can leverage cash value to achieve a balance between protection and wealth accumulation. As the financial landscape evolves, the role of cash value in insurance policies continues to be a dynamic and impactful aspect of holistic financial planning.